2. They’re mistaken for insurance because they often involve payment when things don’t go as planned.

DIFFERENCES BETWEEN SURETY AND INSURANCE

1.Number of parties involved

(i) Surety bonds protect the Obligee. Surety bonds involve 3 people:

-The Obligee - the person who is protected by the bond,

-The Principal - the person who gets the bond

-The Surety - the person who issues/supplies the bond

(ii) Insurance protects the insured. Insurance policies involve 2 people:

- The Insured - the person who is protected by the insurance policy

- The Insurer - the person who provides the insurance policy

2. Losses

(i) Surety bonds are not expected to incur losses. Losses are rare and must be fully paid back by the Principals. Because of this, surety bonds are only issued to individuals who are qualified.

(ii) Insurance comes with expected losses. The insurance company knows this and pools the risk with the law of large numbers so that the risk is shared.

3. Premium Paid

(i) For surety bond premium, the premium paid for a surety bond is for the guarantee that the Principal follows through with their obligation or promise. Premium is paid one time. Premium does not need to be paid again until the bond needs to be renewed (generally one year later).

(ii) For insurance premium, The premium paid for an insurance policy is designed to cover any losses that might happen. Premium is often paid on a monthly basis.

4. Repayment of Claims

(i) When a surety bond claim is paid, the surety company pays the claim. Because of the nature of surety bonds, the surety company requires you to repay every single penny.

(ii) Insurance claims: When an insurance claim is paid, the insurance company pays the claim. They do not expect to be repaid by the Insured, nor is it required.

PRICING

1. Technical Premium = Expected Losses + Expenses + Target Profit

2. Expected losses = frequency x severity

(i) Credit rating (e.g. Moody’s, S&P)

(ii) Experience of management

(iii) Time in business

(iv) Stability of earnings:

(v) Firm – Financial statements, structure of capital

(vi) Industry segment

(vii) Concentration of business

(viii) Partners and exposure in other projects

(ix) Economic Cycle

4. Duration of the risks - Large duration in the life of the policy is very important. Exposure of all policies will change according to lifetime of the project

5. Severity

(i) Severity = Contract Value * Loss Given Default

(ii) Contract Value is s a random variable as the exact amount of exposure at the time of default may be uncertain. The respective maturity profile needs to be reflected in the modelling of the severity component of surety risks.

(iii) Loss Given Default is 1 – Recovery Rate. A Random variable reflects the fraction of the exposure that results in a loss after accounting for any recoveries.

(iv) Severity is the Exposure net of retention, usage and recoveries.

(v) Loss severity depends on the complexity of the underlying project: can the contractor easily be replaced? what are the costs occurring to mitigate the loss? Contract value/exposure, availability of collateral and recovery prospects and Quality of collateral

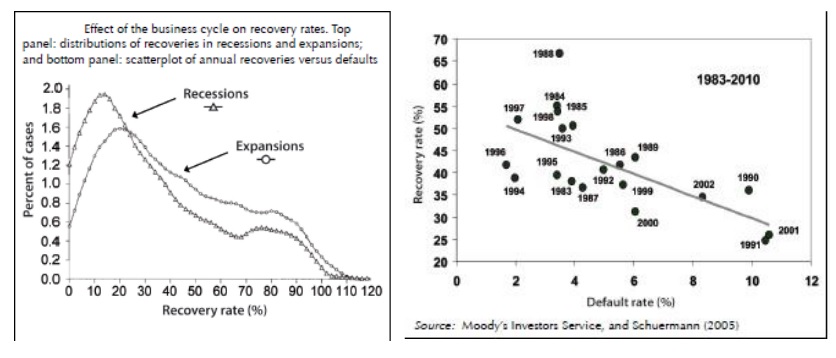

(vi) Recovery rate could change across economic cycle or according to default rate. Examples as follow:

SURETY PRICING FRAMEWORKS - TRADITIONAL ACTUARIAL MODELS

1. They include Experience and exposure rating, Individual and collective models, Aguilar & Gudiño Model

2. Then Net Premium has two components, Cost of financing the claims and cost of the guarantees that will not be recovered

Note:

(i) t1 :

claim date. t2 : guarantee recovery date. T: t2 – t1

(ii) Pt1(r): frequency factor. Probability of

having a claim

(iii) St1: severity factor. Expected claim as

fraction of the exposed surety

(iv) ε: fraction of the claim that will not be recovered

(loss)

(v) i: cost of opportunity of the capital

(vi) r: yield rate of a fixed income instrument

SURETY PRICING FRAMEWORKS - FINANCIAL MARKETS MODEL

1. Insurance and financial markets converge: produces the same risks

2. Severity: using default models from financial markets and adjusting by loss triggers. The expected level of guarantees recoveries is added.

Note:

(i) Ex: exposure

(ii) EDF: probability of claim

(iii) r: recovery rate

(iv) α: probability of claim as a surety product divided by

probability of default as a financial product

SURETY PRICING FRAMEWORKS - PORTFOLIO PRICING

1. Losses won’t be independent (correlation different to zero) as one contractor can be responsible for several projects (accumulation of risks), Economic Cycle can affect several industries and Political Cycle can affect infrastructure projects

Note:

(i) Ultimate Losses = Probability of Default * (Expected Losses + Unexpected Losses + Economic Capital + Expected Shortfall) * (1- Recovery Rate)

(ii) Ultimate Loss Ratio will factor in Estimated Large Losses, Portfolio Diversification, Reinsurance Treaties

2. Unexpected losses are function of standard deviation of severity of single risks (homogeneity of portfolio)

3. Surety portfolios are typically less diversified than other product classes. Traditionally, surety portfolios are concentrated around the construction industry, often with a focus on country specific contractors. The high risk concentration combined with the risk profile, lead to a higher severity risk and hence, are increasing the capital intensity of surety portfolios.

4. By using Montecarlo simulation, it is possible to include deviations with respect to the expected loss that correspond to events occurring frequently

SURETY RESERVING

1. Accident Date

(i) Loss is not typically “fortuitous”

(ii) claim files can open before a claim is made

(iii) Can be outside the “policy period”

2. Offsets include contract balances, indemnity, salvage, and subrogation

(i) Personal indemnity is not uncommon

(ii) Recovery can extend for years

(iii) Usually requires legal process (several years)

THOUGHTS

1. In Addition to frequency and severity, Portfolio Analysis requires

(i) Exposure time of the project

(ii) Correlation between risks (accumulation of exposure) and between industries

(iii) Economic Cycles

(iv) Large Losses / Extreme Events

(v) Long tail claims

2. United States reserving includes the following factors:

(i) Two claim tiers: recent vs. litigation

(ii) Triangular methods limited

(iii) BF & Claims Projection

(iv) Severe events

(v) Offsets

3. United States face the following challenges with data:

(i) Large limits, idiosyncratic losses, correlation, & extreme volatility

(ii) Collateral, Salvage & Subrogation

(iii) Short/Long-tail exposure

(iv) Limited industry data

(v) Multi-year policies

(vi) Occurrence

(Source:Suretysolutionsllc, Society of Actuaries)